Many refinance conversations never turn into applications because the borrower is interested, but not ready. A homeowner may want information about rates, equity, cash-out options, or monthly payments without having a clear decision window. In 2026, that gap between curiosity and intent is widening as more refinance research happens privately through Google, AI search, calculators, and comparison content before a lender is contacted.

For mortgage lenders, this can be frustrating.

The team may stay busy. Calls may come in. Follow-up may happen. Loan officers may work hard. But fewer conversations move into real applications.

When that happens, the problem is not always effort, sales skill, or follow-up cadence.

Often, the problem is timing.

The borrower entered the conversation before their intent was clear, or after they had already formed expectations somewhere else.

The Main Answer: Why Do Refinance Conversations Fail to Become Applications?

Refinance conversations fail to become applications when borrower interest is mistaken for borrower intent. Interest means the homeowner is curious. Intent means the homeowner is actively evaluating whether refinancing makes sense, comparing options, and moving toward a decision.

That distinction matters.

A borrower who asks about rates may not be ready to apply. A borrower who clicks an ad may not understand the financial tradeoffs. A borrower who fills out a form may still be comparing, waiting, or gathering information.

The application usually happens when the borrower has enough clarity, confidence, timing, and trust to move forward.

That clarity often forms before the first call.

Key Takeaways

- Most stalled refinance conversations are caused by weak borrower readiness, not only weak follow-up.

- Borrower interest and borrower intent are not the same.

- Refinance intent often begins during private research before a form fill, call, or quote request.

- The Mortgage Bankers Association forecast refinance originations to increase 9.2% to $737 billion in 2026, which shows refinance activity still exists in a selective market.

- The CFPB says borrowers can potentially save $600 to $1,200 per year by getting mortgage offers from multiple lenders, which reinforces how comparison-driven mortgage decisions are.

- Google AI search features such as AI Overviews and AI Mode are now part of Google Search from a site owner perspective.

- Pew Research Center found that users who encountered a Google AI summary clicked traditional search result links less often than users who did not encounter one.

- Evoltra Solutions helps mortgage businesses and high-trust professional firms become easier to find, trust, and choose across Google, AI search, reviews, website clarity, business profiles, directories, and authority signals.

Why Refinance Calls Feel Busy But Applications Feel Thin

A refinance team can have a full call calendar and still struggle with application volume.

That happens when too many conversations come from borrowers who are curious but not ready.

Common examples include:

- Homeowners reacting to rate headlines

- Borrowers checking whether a lower payment is possible

- Homeowners exploring cash-out options with no clear timeline

- Borrowers comparing refinancing against a home equity line of credit

- Investors gathering general information

- Past clients wondering if now is the right time

- Shoppers asking for a quote without understanding the full decision

These are not bad conversations. They may even become useful later.

But they are not always application-ready.

A borrower can be interested in refinancing without having the urgency, confidence, equity position, savings threshold, or financial reason needed to move forward.

That is why call volume alone can be misleading.

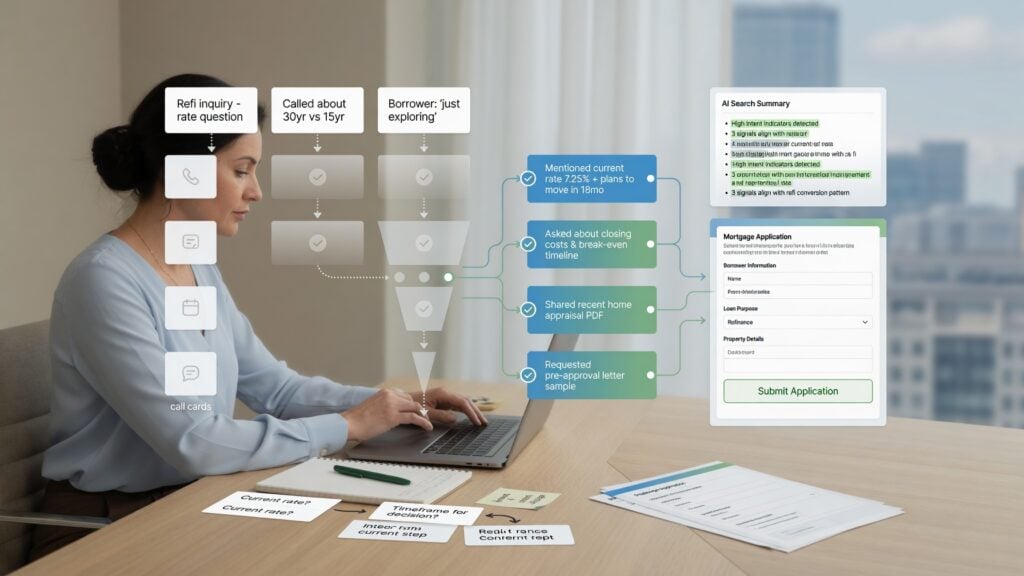

Interest Is Not the Same as Refinance Intent

Interest is broad. Intent is specific.

Interest sounds like:

- “I’m just checking rates.”

- “I wanted to see if refinancing makes sense.”

- “I’m curious about cash-out.”

- “I heard rates might change.”

- “I’m not sure yet.”

Intent sounds more focused:

- “I want to compare a cash-out refinance against a HELOC.”

- “I need to know my break-even point.”

- “I want to reduce my payment if the math works.”

- “I’m consolidating debt and need to understand my options.”

- “I’m comparing Loan Estimates from a few lenders.”

- “I plan to make a decision within a specific timeframe.”

The difference is not just tone. It is readiness.

Traditional lead sources often blur that distinction. A form fill may look like intent, but it may only represent curiosity. A rate inquiry may look like a buying signal, but it may simply be early research.

For refinance lenders, that distinction affects everything: intake, follow-up, forecasting, team capacity, and application conversion.

Why Borrowers Stall After the First Conversation

Borrowers often stall after the first refinance conversation because they are still trying to understand the decision.

Refinancing is not a simple product choice. It can affect monthly payment, interest paid over time, loan term, cash flow, equity, closing costs, and long-term financial planning.

The CFPB’s Loan Estimate guidance tells borrowers to request multiple Loan Estimates so they can compare and choose the loan that is right for them.

That means borrowers may pause after a call to compare, recalculate, ask someone else, or keep researching.

A stalled conversation may mean:

- The borrower does not understand the benefit clearly.

- The monthly savings are not strong enough.

- The closing costs feel unclear.

- The timeline is not urgent.

- The borrower is comparing other lenders.

- The borrower needs more trust before applying.

- The borrower was never truly application-ready.

The lender may interpret the stall as a sales problem. In many cases, it is an intent problem.

Where Refinance Intent Actually Shows Up

Refinance intent often appears before the call.

It shows up when borrowers search for specific questions, compare scenarios, and try to understand financial tradeoffs.

Intent may appear in searches like:

- “cash-out refinance vs HELOC”

- “does refinancing make sense if rates are higher”

- “how to calculate refinance break-even”

- “refinance closing costs”

- “how much equity do I need to refinance”

- “should I refinance to consolidate debt”

- “when is refinancing worth it”

- “compare mortgage refinance lenders”

These searches are different from broad curiosity.

They show a borrower trying to evaluate a decision.

In 2026, some of this behavior happens inside AI-powered search experiences. Google’s Search Central guidance explains that AI features such as AI Overviews and AI Mode are part of the Google Search experience and may show AI-generated responses with links.

That matters because a borrower may form an opinion before clicking a lender’s website or speaking to a loan officer.

Why AI Search Changes Application Quality

AI search changes application quality because it changes what borrowers know before they reach out.

A borrower may use AI search to understand refinance options, compare loan types, evaluate cash-out scenarios, or decide whether a lower payment justifies the cost. That education can happen privately and quickly.

Pew Research Center found that Google users who encountered an AI summary clicked a traditional search result link in 8% of visits, compared with 15% of visits when no AI summary appeared.

For mortgage lenders, the practical point is simple: some borrower education now happens without a website visit.

That means lenders may not see the earliest signals in standard website analytics. The borrower may be researching, comparing, and narrowing options before the lender ever sees a lead.

If the lender is not visible during that early research stage, the first call may begin without enough recognition or trust.

Why More Leads Do Not Always Create More Applications

More leads do not always create more applications because low-intent volume creates noise.

A lender can increase lead flow and still see weak application conversion if the borrowers are not ready.

More low-intent leads can create:

- More unproductive intake calls

- More follow-up with no response

- More borrowers who only want a rate quote

- More pricing objections

- More confusion around closing costs

- More fallout after initial conversation

- More strain on loan officers

- Less time for high-intent opportunities

This is why lead quality matters more than lead quantity.

The issue is not whether a borrower has any interest in refinancing. The issue is whether the borrower is close enough to a decision for a lender conversation to be productive.

Why Visibility Timing Matters

Visibility timing matters because borrowers form expectations before they contact a lender.

If a borrower encounters helpful, clear, credible information early, the first conversation may begin with more confidence.

If the borrower only finds generic refinance pages, lead forms, rate ads, or unclear explanations, they may enter the call less prepared.

That changes the conversation.

A borrower with clearer intent may ask better questions, understand tradeoffs, and move toward an application more efficiently.

A borrower with weak intent may need more education, more reassurance, and more follow-up before deciding whether refinancing is even relevant.

The difference is not always the loan officer.

It is often the quality of visibility before the call.

The Hidden Cost of Premature Refinance Conversations

Premature refinance conversations feel productive because they create activity. But they often carry hidden costs.

They can reduce team efficiency. They can make forecasts less reliable. They can create frustration for loan officers who are doing everything right but speaking with borrowers too early.

The hidden costs include:

- Time spent educating borrowers who are not ready

- More follow-up tasks with low probability

- Lower application-to-conversation ratios

- Less attention for stronger opportunities

- More inconsistent pipeline reporting

- Higher cost per funded loan

- More pressure to buy or generate even more leads

This is why refinance teams should look beyond call count.

A high volume of early-stage conversations may look like demand, but it may not behave like demand.

What Better Refinance Conversations Have in Common

Better refinance conversations usually start with more context.

The borrower may already understand why they are calling. They may know what decision they are trying to make. They may have a reason for acting, a rough timeline, or a specific scenario they want to evaluate.

A stronger refinance conversation often includes:

- A clearer borrower goal

- A specific financial reason

- A real comparison point

- A more realistic timeline

- Better awareness of costs

- More trust in the lender

- A stronger sense of what happens next

This does not guarantee an application. No visibility strategy can guarantee that.

But it improves the quality of the conversation.

What Lenders Should Review at a High Level

This is not a detailed DIY checklist or implementation roadmap. But refinance lenders should understand the areas that may be affecting application conversion.

At a high level, lenders should review whether their online presence supports:

- Borrower readiness

- Refinance scenario clarity

- AI search visibility

- Google search visibility

- Website service clarity

- Refinance educational content

- Google Business Profile accuracy

- Review trust signals

- Local or regional relevance

- Business profile consistency

- Branded search confidence

- Clear next steps for informed borrowers

The goal is not to solve every application-conversion question in one article.

The goal is to identify whether the lender is visible early enough to help borrowers move from interest to intent.

Why This Is Not Just a Sales Problem

When refinance conversations do not turn into applications, it is easy to blame sales process.

Sometimes sales process matters. But in many cases, the issue starts before the first conversation.

The borrower may not understand the refinance decision. The borrower may not trust the lender yet. The borrower may be comparing too many options. The borrower may be responding to a headline instead of a real financial need.

That is not just a sales problem.

It is a visibility, timing, and intent problem.

Mortgage lenders should not only ask, “How do we follow up better?”

They should also ask, “Are we appearing when borrowers are forming intent?”

How Evoltra Solutions Helps

Evoltra Solutions helps mortgage businesses and high-trust professional firms become easier to find, trust, and choose across Google, AI search, reviews, website clarity, business profiles, directories, and online authority signals.

For refinance-focused lenders, Evoltra looks at how borrowers may encounter the business before the first call. That includes Google visibility, AI search visibility, refinance content, reviews, service pages, business profiles, and trust signals.

Evoltra does not promise rankings, AI recommendations, lead volume, applications, funded loans, or immediate results. Those outcomes cannot be guaranteed.

The focus is clarity, visibility, and trust.

The goal is to help lenders understand whether their online presence supports better borrower intent before the conversation begins.

Final Thoughts: Applications Start Before the Application

Most refinance conversations do not fail because lenders are not trying hard enough.

They fail because borrower intent is not clear enough when the conversation happens.

A homeowner may be interested, curious, or rate-sensitive without being ready to apply. The lender’s job becomes harder when that borrower reaches out before they understand the decision, or after they have already formed expectations elsewhere.

In 2026, refinance application quality depends on more than lead volume.

It depends on whether borrowers can find clear, trustworthy information while they are still researching. It depends on whether the lender is visible in Google and AI search before the first call. It depends on whether the borrower arrives with enough confidence to move from conversation to application.

Better applications begin with better intent.

And better intent often begins long before the lender sees the lead.

FAQs

Why do refinance conversations not turn into applications?

Refinance conversations often do not turn into applications because the borrower is interested but not ready. They may be exploring rates, comparing options, or gathering information without a clear decision window.

What is the difference between refinance interest and refinance intent?

Refinance interest means a borrower is curious about refinancing. Refinance intent means the borrower is actively evaluating a refinance decision, comparing options, and moving closer to applying.

Why do refinance borrowers stall after the first call?

Borrowers may stall after the first call because they need more clarity on costs, savings, timing, loan terms, or lender trust. They may also be comparing multiple lenders before deciding whether to apply.

How does AI search affect refinance application quality?

AI search affects refinance application quality because borrowers can research refinance questions before contacting lenders. They may form expectations, compare options, and decide whom to trust before visiting a lender’s website or speaking with a loan officer.

Why does lead volume not always create more applications?

Lead volume does not always create more applications because many leads may be low-intent, poorly timed, or still in the research stage. More activity can create more calls without improving application conversion.

What are high-intent refinance leads?

High-intent refinance leads come from borrowers who are actively evaluating a refinance decision. They usually have a clearer reason, stronger timeline, more specific questions, and greater readiness than borrowers who are only casually exploring.

Can better visibility guarantee more refinance applications?

No. Better visibility cannot guarantee more refinance applications, rankings, AI mentions, leads, or funded loans. It can help lenders identify whether their online presence supports borrower readiness before the first conversation.

What should lenders measure besides call volume?

Lenders should look at borrower readiness, conversation quality, application conversion, AI search visibility, Google visibility, branded search confidence, review trust signals, and cost per funded loan.